No Tax on Overtime 2026: What Every US Worker Needs to Know

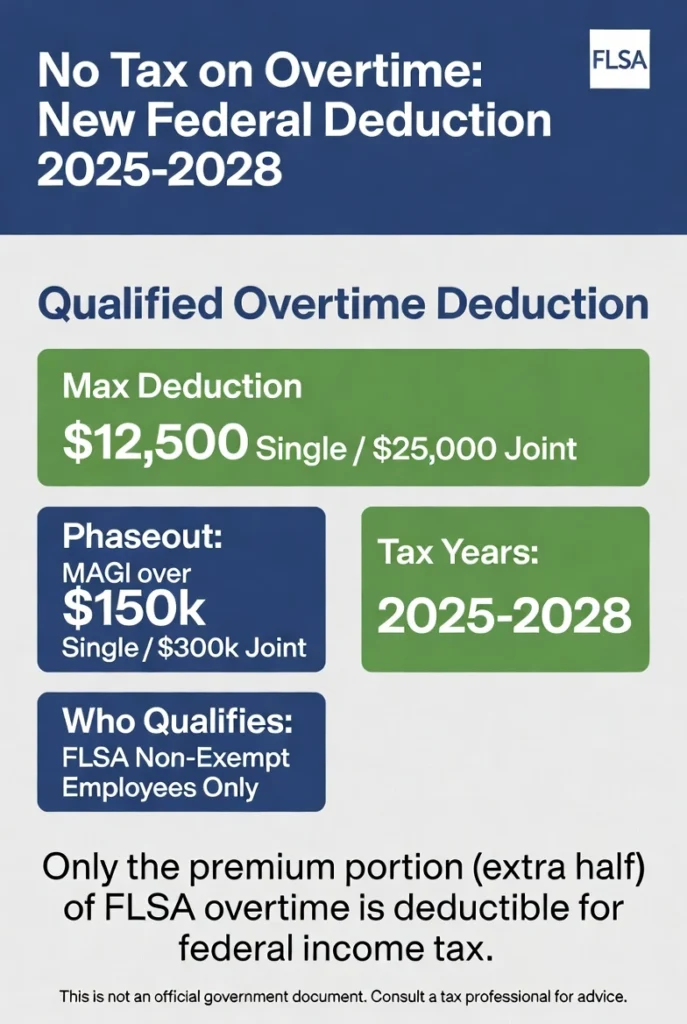

Quick Answer: The No Tax on Overtime deduction allows eligible FLSA non-exempt workers to deduct up to $12,500 (single) or $25,000 (joint) of overtime premium pay from federal taxable income for tax years 2025–2028. Only the premium portion above regular rate qualifies, not the full overtime paycheck.

You put in the extra hours. You worked through the weekend, stayed late on Thursday, covered a shift nobody else wanted. And then the paycheck came and overtime got taxed just like everything else. For the first time in decades, that calculation is changing.

The federal government passed a new law that lets eligible workers deduct part of their overtime pay from federal taxable income. It is not a complete exemption and it does not apply to everyone. But if you work overtime covered by the Fair Labor Standards Act, this new rule may put real money back in your pocket when you file.

| Max Deduction | Income Phaseout | Tax Years | Who Qualifies |

|---|---|---|---|

| $12,500 single $25,000 joint | MAGI over $150,000 $300,000 joint | 2025 through 2028 | FLSA non-exempt employees only |

Table of Contents

What the Law Actually Does on Overtime

The One Big Beautiful Bill Act, passed in 2025 and signed into law as P.L. 119-21, added a new federal income tax deduction for what the IRS calls qualified overtime compensation. The phrase no tax on overtime gets repeated a lot but it overstates what the law does.

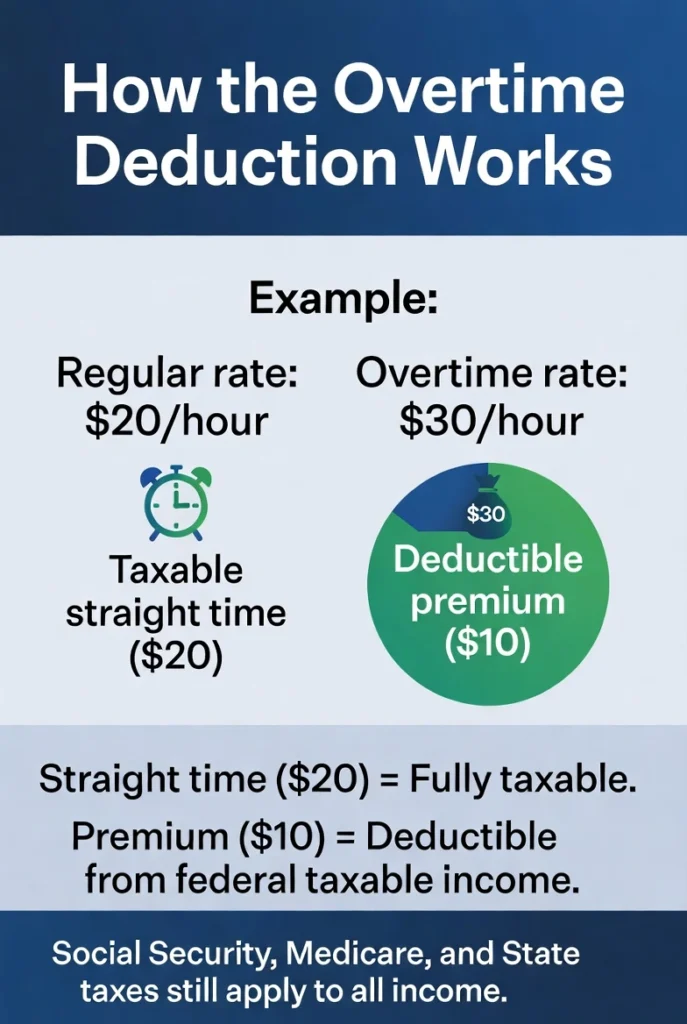

Under this law, if you receive qualified overtime compensation, you may deduct the pay that exceeds your regular rate of pay. That means only the premium portion, not your full overtime paycheck. Here is how it works in plain numbers: you earn $20 per hour.

For overtime hours you receive $30 per hour. The $20 straight time portion is still fully taxable. Only the extra $10, the premium portion, qualifies for the deduction. Social Security, Medicare, and state income taxes still apply to all overtime pay. The deduction only reduces your federal taxable income.

Who Qualifies for No Tax on Overtime

You qualify if all of these are true: you are a non-exempt employee covered by the FLSA, your overtime comes from the federal FLSA requirement rather than only from state law or a union contract, you have a valid Social Security number, and if you are married you file jointly.

You do not qualify if you are exempt under the FLSA, meaning you pass the salary level, salary basis, and duties tests. State-mandated overtime, holiday pay, weekend differentials, and overtime from collective bargaining agreements generally do not qualify for the deduction even if they result in higher pay.

These Types of Overtime Do NOT Qualify:

X State-mandated overtime that exceeds FLSA requirements

X Holiday pay and weekend differentials

X Overtime negotiated in a union contract beyond FLSA

X Double time paid for reasons other than crossing 40 hours under FLSA

X Discretionary bonuses your employer pays voluntarily above FLSA

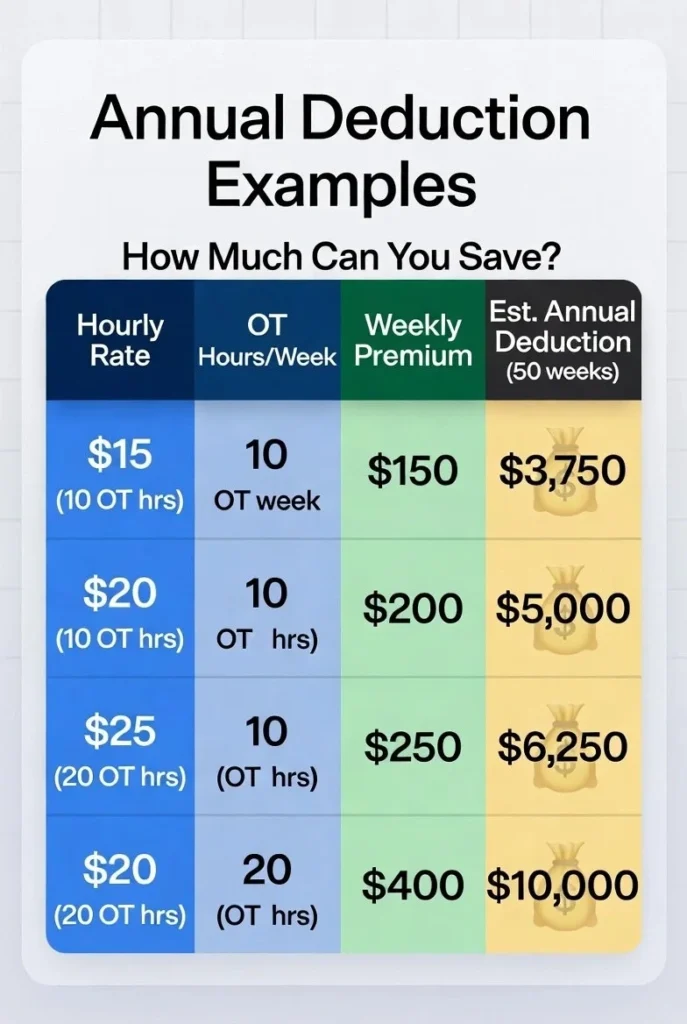

How Much Can You Deduct Tax on Overtime

The maximum annual deduction is $12,500 per return, or $25,000 if you file jointly. The deduction phases out if your modified adjusted gross income is over $150,000, or $300,000 if you file jointly. The deduction is available whether you take the standard deduction or itemize. You claim it on Schedule 1-A, Form 1040.

| Hourly Rate | Overtime Hours | Weekly Premium | Annual Deduction |

|---|---|---|---|

| $15/hr | 10 hrs OT | 10 x $7.50 = $75 | ~$3,750 |

| $20/hr | 10 hrs OT | 10 x $10 = $100 | ~$5,000 |

| $25/hr | 10 hrs OT | 10 x $12.50 = $125 | ~$6,250 |

| $20/hr | 20 hrs OT | 20 x $10 = $200 | ~$10,000 |

Premium = 0.5 x regular hourly rate. Annual estimates assume 50 working weeks.

deduction for qualified overtime compensation under FLSA, effective

for tax years 2025 through 2028.

Eligible workers can deduct up to

$12,500 per return.

overtime paycheck. Social Security

and Medicare taxes still apply.

When It Started and How Long It Lasts

The deduction applies retroactively starting January 1, 2025. That means overtime hours worked all year in 2025 qualify even though the law passed mid-year. The current law is set to expire after 2028 unless Congress acts to extend it. You have four tax years to take advantage of this deduction: 2025, 2026, 2027, and 2028.

How to Claim It

Tax year 2025 has a special situation. Because the law passed mid-year, employers were not required to separately report qualified overtime compensation on 2025 W-2 forms. The IRS allows several methods to calculate your deductible amount using pay stubs, year-end payroll summaries, or employer statements.

The basic calculation: multiply your overtime hours by your regular hourly rate, then multiply by 0.5 to get the premium portion that qualifies.

For tax year 2026 and forward, employers are required to separately report qualified overtime compensation on Form W-2, Box 12, using Code TT. This makes the calculation straightforward directly from your W-2.

Why Your Timecard Records Matter More Now

To claim the deduction accurately, especially for 2025 where employers were not required to break out overtime separately, you need your own records showing the hours you worked and which of those hours were overtime. A weekly PDF export from a time card calculator gives you that record.

When your W-2 arrives or when your employer provides a payroll summary, you can cross-check those numbers against your own documentation. Track and verify your overtime hours free at timecardscalculator.com. Export a PDF record every week and keep it with your pay stubs. No signup required. No cost.

Quick Reference table to understand the term “No Tax on Overtime”

Most workers spend more time confused about this deduction than it takes to actually claim it. The rules sound complex but the math is straightforward once you know what qualifies & what does not. Every number in this table comes directly from IRS official guidance. No interpretation, no guesswork. If your situation matches the eligibility criteria, the deduction is yours to claim. Use it before you file.

| What You Need to Know | The Answer |

|---|---|

| What qualifies | FLSA overtime premium only — the half in time-and-a-half |

| Maximum deduction | $12,500 single filer / $25,000 married filing jointly |

| Income phaseout | Starts at $150,000 MAGI / $300,000 for joint filers |

| Tax years covered | 2025 through 2028 |

| Where to claim it | Schedule 1-A, Form 1040 |

| 2025 W-2 reporting | Not required — use pay stubs to calculate |

| 2026 W-2 reporting | Required — Box 12, Code TT |

| State taxes | Not affected — federal income tax deduction only |

| Social Security and Medicare | Still apply to all overtime pay |

Frequently Asked Questions – FAQs

These questions are based on official IRS guidance and the most common points of confusion workers face when claiming the qualified overtime compensation deduction.

Does no tax on overtime mean my overtime pay is completely tax free?

No. The law created a federal income tax deduction for the premium portion of FLSA overtime only. Social Security, Medicare, and state income taxes still apply to all overtime pay. Your federal income tax bill goes down but overtime is not fully exempt from taxation. The deduction applies only to the half portion of time-and-a-half pay that exceeds your regular rate.

I work in California and get daily overtime after 8 hours. Does that qualify?

Only the portion of your California overtime that is also required by the federal FLSA qualifies. Hours beyond 40 in a workweek qualify under federal law. Daily overtime after 8 hours that does not push your weekly total past 40 hours may not qualify because it is required by California state law rather than by the FLSA. Each workweek needs to be evaluated separately. See the California Overtime guide at timecardscalculator.com/California-overtime for how California rules interact with federal FLSA requirements.

My employer did not show overtime separately on my 2025 W-2. Can I still claim the deduction?

Yes. The IRS allows workers to calculate their qualified overtime using pay stubs, payroll summaries, or other employer records for the 2025 tax year. Use your own time records to identify overtime hours and multiply those hours by half your regular hourly rate to find the deductible premium amount. Starting with tax year 2026, employers are required to separately report qualified overtime in Box 12, Code TT on your W-2. 4 I am a salaried employee.

Do I qualify for this deduction?

It depends on your FLSA classification. Salaried non-exempt employees who receive FLSA overtime do qualify. Salaried exempt employees who pass the duties test and meet the salary threshold do not qualify because they are not entitled to overtime under the FLSA in the first place. Your classification, not your pay structure, determines eligibility. Check your exempt vs non-exempt status at timecardscalculator.com/exempt-vs-non-exempt before assuming either way.

Does the deduction apply to overtime worked on holidays or weekends?

Not automatically. Holiday pay and weekend differentials do not qualify unless those hours also pushed your total workweek beyond 40 hours and the extra pay was required by the FLSA specifically. Voluntary employer premiums for holidays and weekend pay that exceeds FLSA requirements are not qualified overtime compensation under the law.

How long does this deduction last?

The current law covers tax years 2025 through 2028. After that the deduction expires unless Congress passes a new law to extend it. You have four years to take advantage of this deduction. Track your overtime hours carefully each year and keep your timecard records as supporting documentation for each filing season.

Where exactly do I claim this on my tax return?

You claim it on Schedule 1-A, Form 1040, which the IRS created specifically for the new deductions under the One Big Beautiful Bill Act. For tax year 2025 you calculate the amount using IRS instructions and pay stubs. For tax year 2026 and forward, your employer will report your qualified overtime in Box 12, Code TT on your W-2, which makes the calculation straightforward.

I am a freelancer or independent contractor. Do I qualify?

Most independent contractors do not qualify because the deduction requires overtime that is mandated under the FLSA, which generally applies to employees rather than contractors. The IRS has noted this is a gray area and further guidance may be forthcoming. If you receive a Form 1099 and believe you may qualify, consult a qualified tax professional before claiming the deduction.

What if my employer paid me more than time-and-a-half for overtime?

Only the portion of your overtime pay that the FLSA requires qualifies for the deduction. If your employer pays double time or a higher rate than FLSA mandates, the deductible amount is still limited to the standard FLSA premium, which is 0.5 times your regular rate. Any additional amount your employer voluntarily pays above the FLSA requirement does not qualify.

Does overtime from state law like Colorado daily overtime qualify?

Only the portion that is also required by the federal FLSA qualifies. Colorado has its own daily overtime rules that can trigger overtime before the 40-hour federal threshold. Hours that push your weekly total above 40 qualify under FLSA. Daily overtime hours that do not reach 40 weekly hours are Colorado-mandated, not FLSA-mandated, and generally do not qualify for the federal deduction. Each week should be evaluated on its own.

Disclaimer:

This guide is for informational purposes only & does not constitute tax or legal advice. Tax laws change & individual circumstances vary. The information in this guide is based on IRS guidance available as of May 2026. For your specific situation, consult a qualified tax professional or visit irs.gov for official guidance.

NOTE: For your specific tax situation, consult a qualified tax professional. GOV IRS Official FAQ

Related Free Tools & Guides are available to understand time cards/ timesheets based on military time & California overtime.

{kind=link}